Raising the Bar on Non-Operated Joint Venture Influencing

Observations from Water Street’s ninth annual London roundtable on JV portfolio governance.

Automakers are pouring billions into new electric vehicle factories, as well as using their deep pockets to secure critical minerals, develop new battery technologies, and build new charging infrastructure. As automakers step outside of their core manufacturing competencies, they are using joint ventures and partnerships at an unprecedented rate.

JUNE 2023 – Road transportation accounts for approximately 15% of global carbon dioxide emissions, primarily due to passenger vehicles. The move to decarbonize passenger vehicles by transitioning to battery electric vehicles (EVs) is transforming the global auto industry. From 2017 to 2022 alone, annual worldwide electric vehicle sales volume soared from approximately 1.5 million to over 10 million. The number of EV charging points in the U.S. and Canada increased threefold in the same 5-year period to 150,000. As the industry grapples with challenges from the growing popularity of EVs, automakers are turning to joint ventures and partnerships to scale up EV production and infrastructure.

The adoption of EVs is rising sharply as governments, investors, and consumers push for more sustainable mobility. But despite the benefits of EVs and the favorable growth outlook, transforming the sector involves significant challenges, including sourcing critical raw materials like lithium and nickel, developing and manufacturing new battery technology, and building new charging infrastructure.

Tesla, a first mover in the industry, addressed these challenges by creating a vertically integrated supply chain, spanning from battery production to electric motor development. Tesla also built a proprietary charging network to support its customers. This strategy contrasted with the decades-long automotive industry trend of focusing on design and outsourcing manufacturing, but was critical to Tesla’s disruption of the industry.

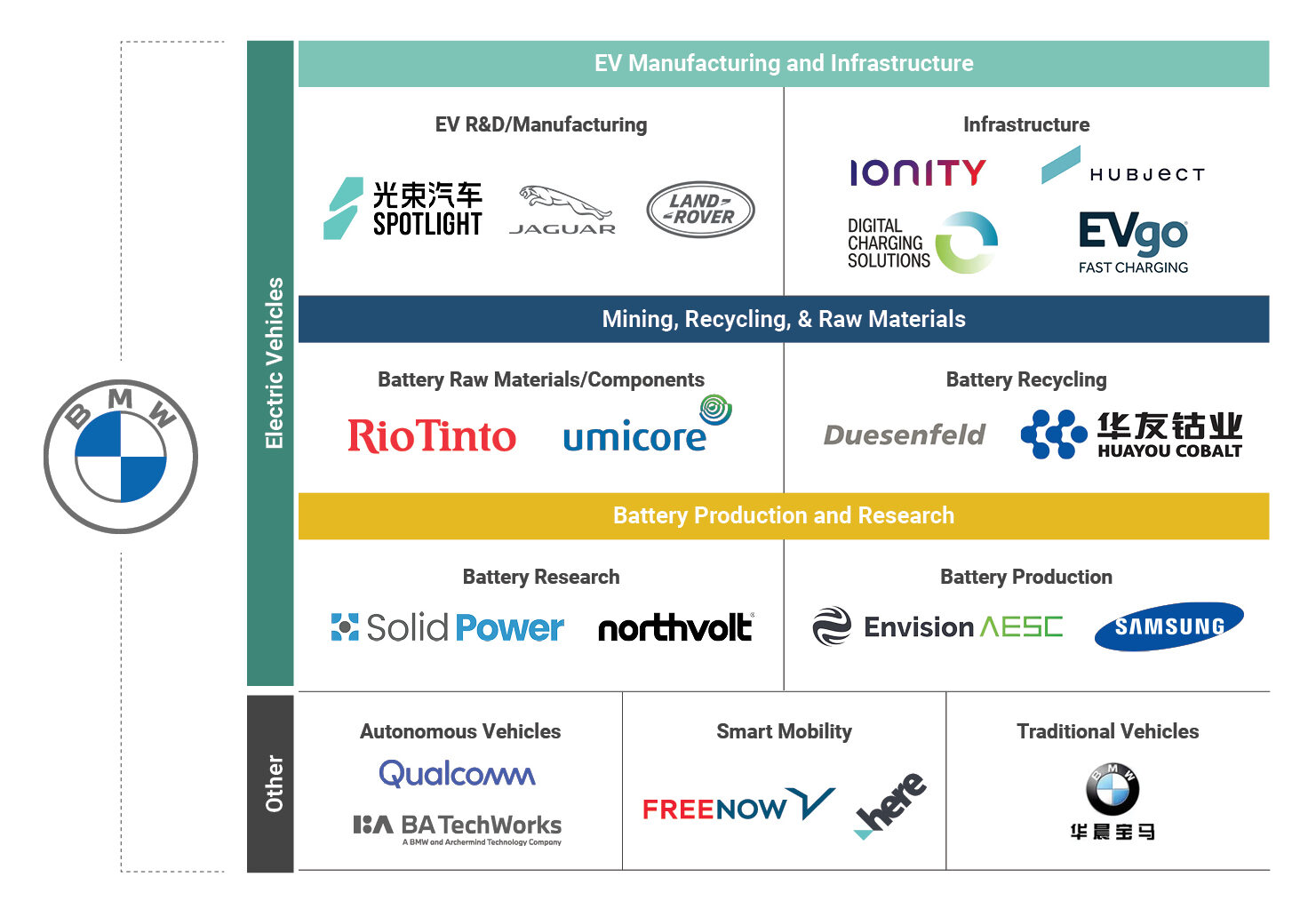

While Tesla is no longer alone in the EV race, the rest of the automotive industry is pushing to catch up. In particular, traditional automakers are increasingly turning to joint ventures and partnerships to spread considerable capital requirements, leverage distinctive partner capabilities, and reduce downside risk.[1]For more on the reasons to enter into joint ventures, see Tracy Branding Pyle, “Why Joint Ventures?” The Joint Venture Alchemist, February 2022, … Continue reading (See Exhibit 1 for an example of how one automotive company, BMW, is using partnerships across its value chain.)

© Ankura. All Rights Reserved.

The 2020s will be a decade of transition to EVs, driven by a combination of government regulation, consumer demand, and industry ambition. Of the three, government regulation is creating the most urgency. For example, the European Union has adopted a mandate to eliminate carbon dioxide emissions from vehicles by 2035, while government regulations in the U.S. will necessitate that 67% of new light-duty vehicles sold by 2032 are electric.

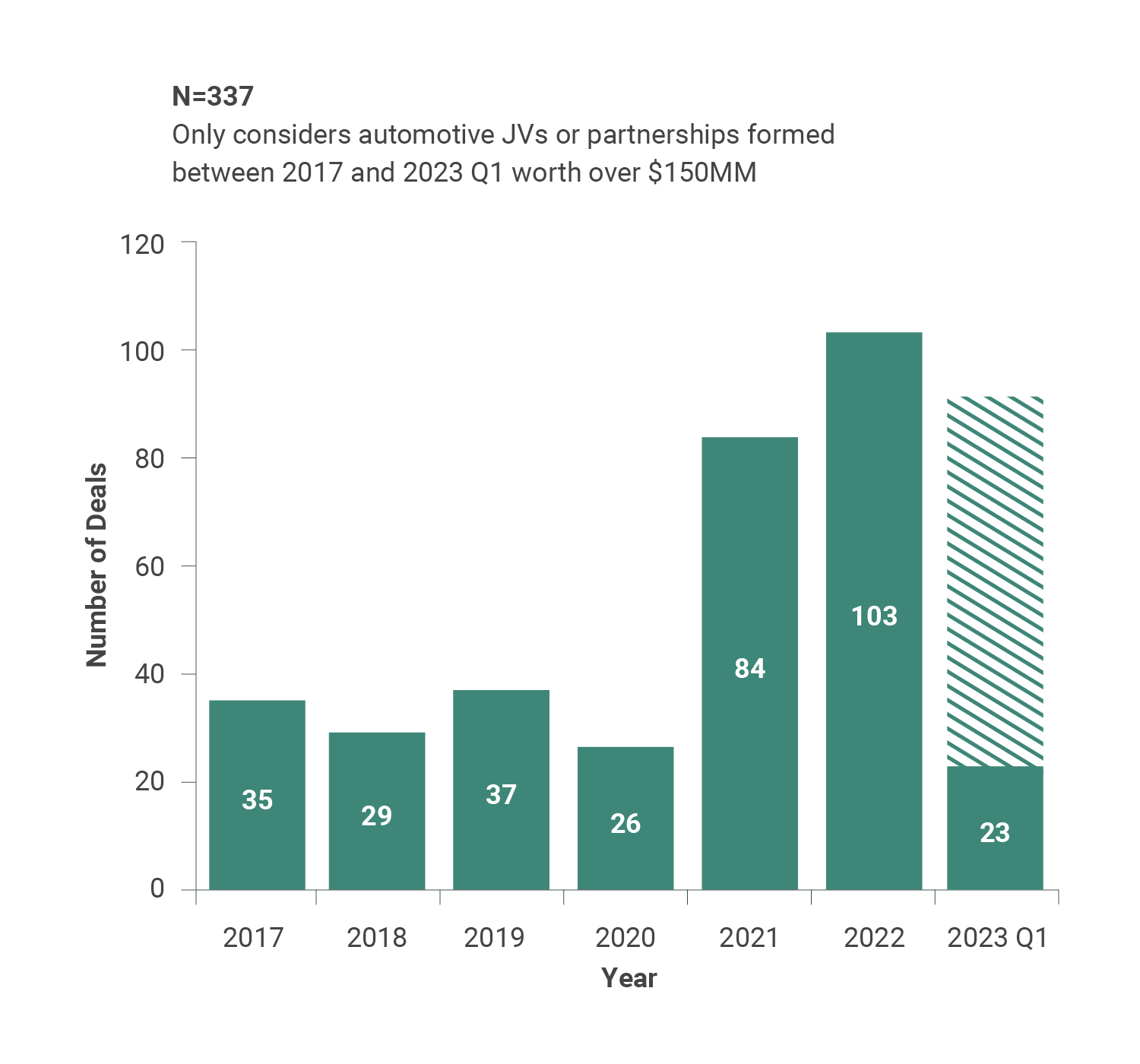

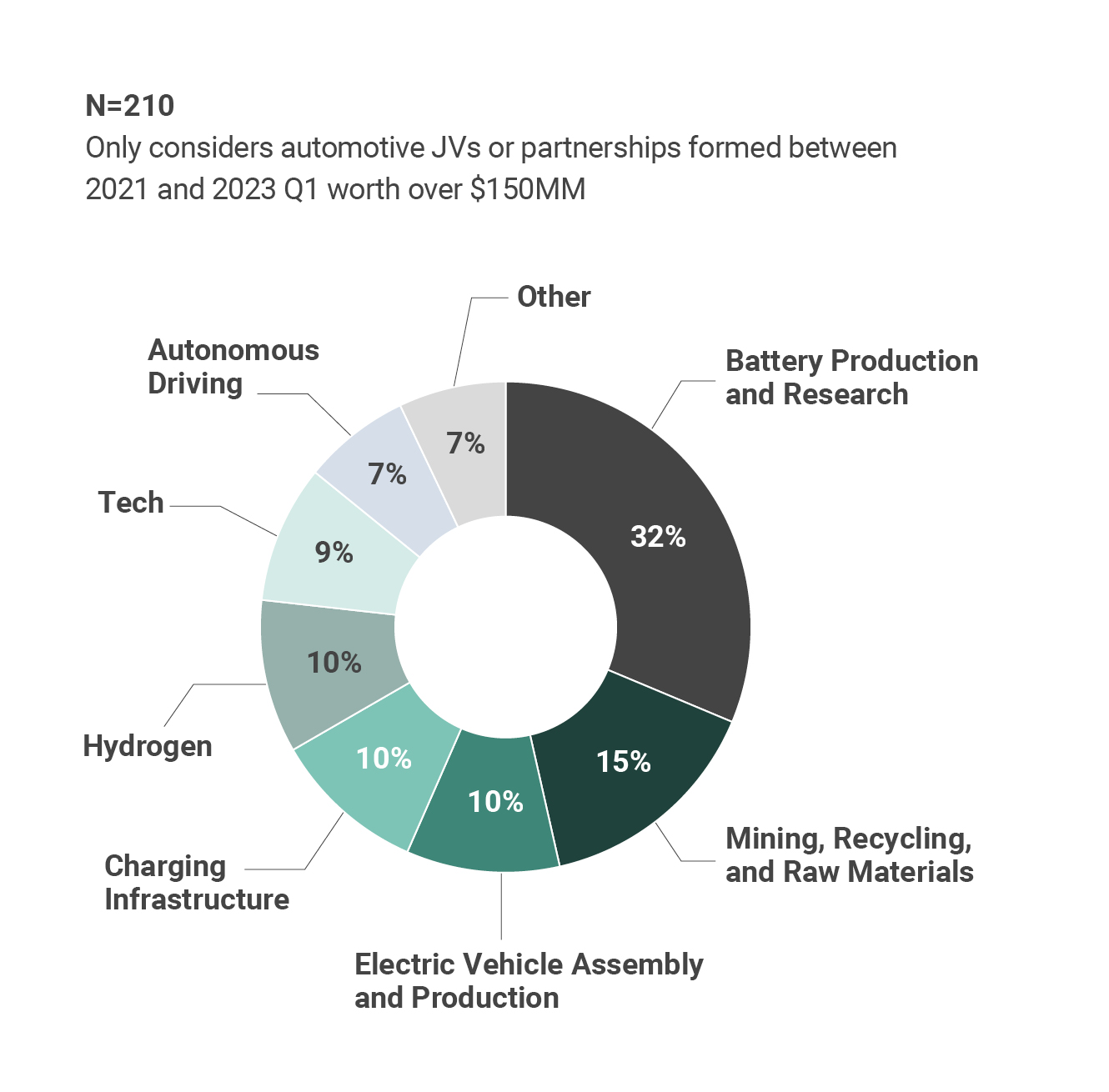

To meet these ambitious timelines, the automotive industry is seeing a surge in partnering deal volume (see Exhibit 2). Deal volume more than doubled from 2019 to 2021 and has remained at a high level since. The increased deal volume has been in nearly every part of the value chain (see Exhibit 3), and activity has been concentrated in these three “hotspots:”

Securing supply of critical materials, including lithium, copper, and nickel

Researching and developing new battery technologies, manufacturing batteries and battery components

Researching and developing new battery technologies, manufacturing batteries and battery components

© Ankura. All Rights Reserved.

© Ankura. All Rights Reserved.

Out of the 210 new, large automotive partnerships established between 2021 and the first quarter of 2023, 15% were in the mining, recycling, and raw materials space. Ensuring a ready supply of critical minerals for batteries is a major priority for automotive companies. For that reason, a growing number of automakers are investing in the mining industry to ensure exclusive or priority access to the metal offtake. One example is General Motors’ (GM) $650 million equity investment in Lithium Americas, which will fund joint development of the Thacker Pass lithium mine in Nevada. GM secured exclusive access to the first phase of production from the mine, and the right of first offer on the second phase of production. Similarly, Mercedes-Benz established a supply partnership with Canadian-German Rock-Tech Lithium to source battery-grade lithium hydroxide.

An additional driver of automotive-mining partnerships is the U.S. Inflation Reduction Act (IRA). The IRA grants vehicle tax credits for EVs that have at least 40% of their battery minerals mined and processed in the U.S. (or in free trade partner countries), or recycled in North America. This requirement will gradually rise to 80% by 2026. Even when the Thacker Pass mine and other mines in development become fully operational, it is expected that the supply of newly mined critical minerals that qualify for the IRA tax credit will still be insufficient to meet demand. This is spurring automakers to partner with and, in some cases, invest in companies like Redwood Materials and Ascend Elements that can take end-of-life batteries and recycle them down to their base metals. These base metals can then be incorporated into future batteries.

As competition for scarce critical minerals increases, we foresee additional automotive investment in mining and recycling companies as well as operational mines — in fact, Volkswagen’s PowerCo battery subsidiary recently announced that it plans to invest in mines directly. Meanwhile, other automotive companies are reportedly interested in buying a minority stake in Vale’s base metals spinoff.

© Ankura. All Rights Reserved.

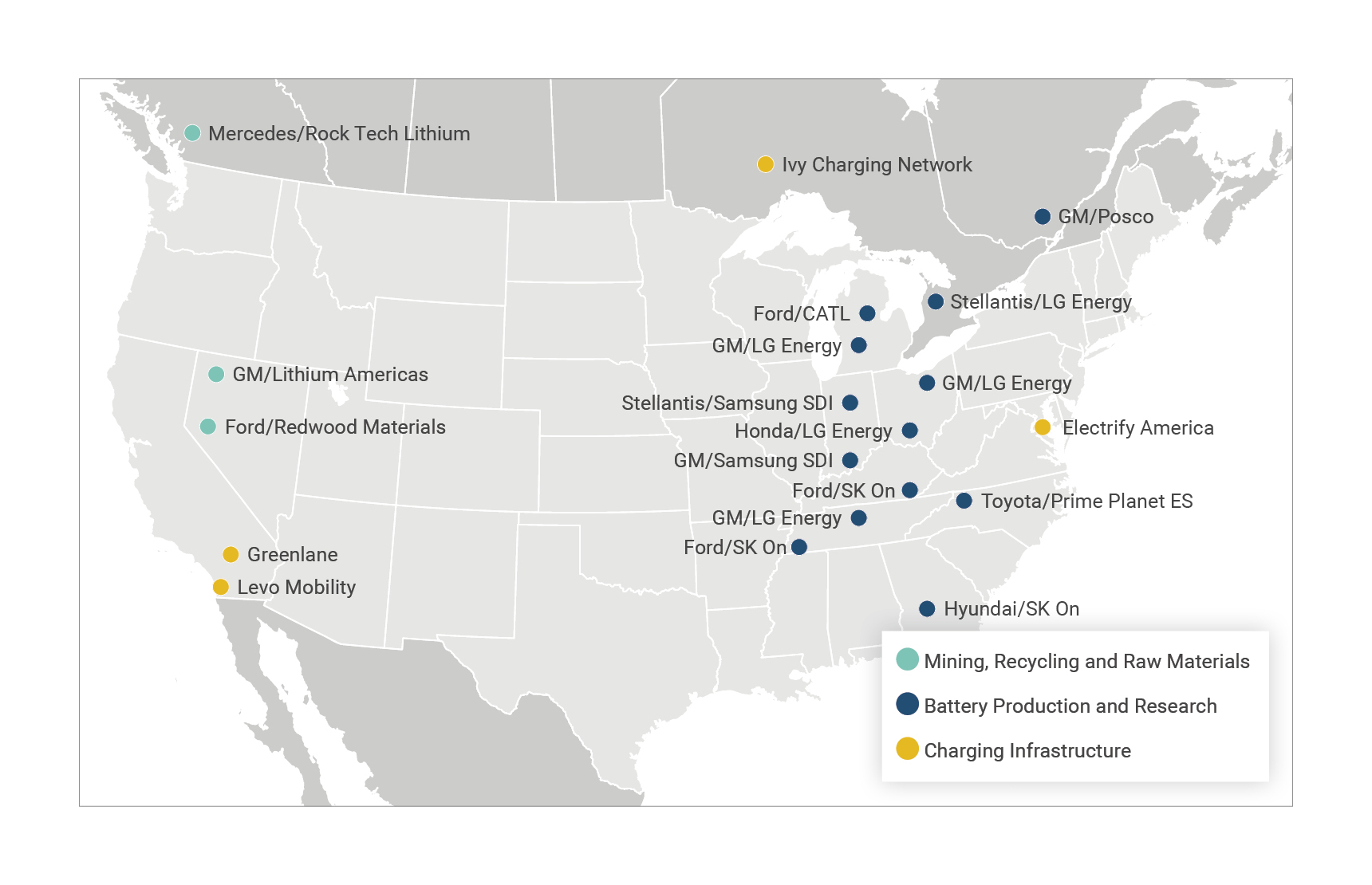

Batteries are simultaneously the most expensive, most complex, and most important components of any EV. Unsurprisingly, the most sizable growth in automotive partnership activity has been in battery supply chains, as automakers push to secure control of both the development and production of battery cells. Tesla, BMW, and Volkswagen were first movers in setting up battery partnerships: Tesla and Panasonic partnered to build a battery manufacturing plant in 2014, BMW teamed up with Solid Power in 2017 to develop solid-state battery technology, and Volkswagen formed a 50/50 joint venture with Northvolt in 2019. Since then, deal activity in the battery space has taken off, with more than a dozen battery technology joint ventures formed between automakers and Asian battery companies to build plants in the U.S. (see Exhibit 4). Geopolitical concerns are also driving non-traditional deal structures — Ford’s partnership with Contemporary Amperex Technology Co. Ltd. (CATL) has Ford owning and operating the manufacturing plant, while CATL will license its battery technology to Ford and provide supporting staff, but CATL will not have an equity stake.

Considering the high capital cost and complex knowhow required to produce batteries, we expect high levels of battery joint venture activity to continue in the upcoming years, with much of that happening in North America as a result of the significant incentives offered by the IRA. In the first quarter of 2023 alone, we have seen new U.S.-based joint ventures announced by Hyundai and SK On, Honda and LG Energy, and GM and Samsung SDI, in addition to European joint ventures announced by Volkswagen and Umicore, as well as Ford, LG Energy and Koç Holdings.

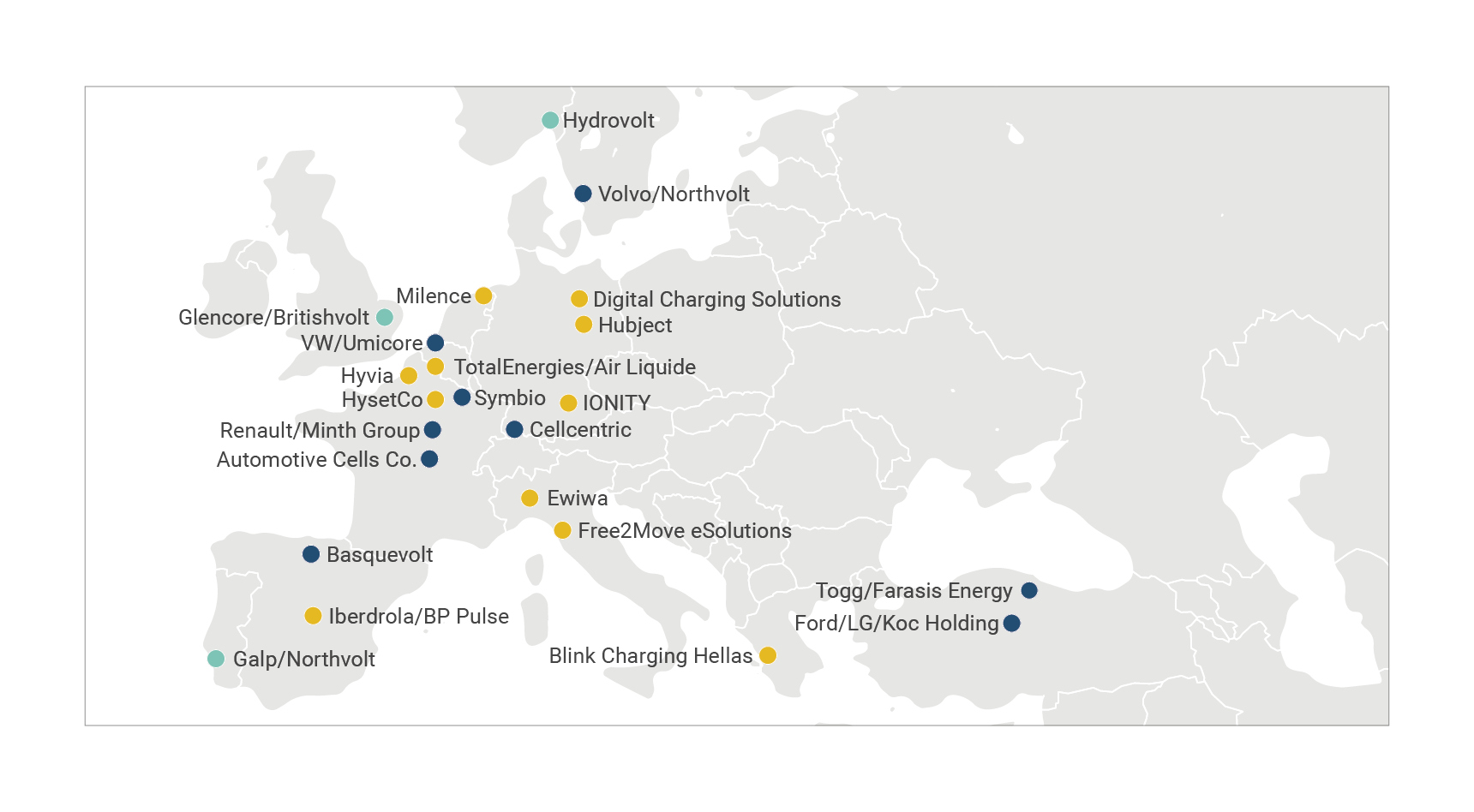

As EVs become ever-more prevalent, the development of public charging infrastructure will be critical. This infrastructure will be key to addressing consumer “range-anxiety” as well as facilitating EV adoption among apartment dwellers and street-side parkers. This too is an area where joint ventures and partnerships have played, and will continue to play, an important role in the cost-effective transition to net-zero (see Exhibit 5). One example is IONITY, a European high-power charging station network joint venture founded in 2017 and currently owned by BMW, Hyundai, Mercedes, Ford, Volkswagen/Porsche, and Blackrock. More recently, Daimler Truck, NextEra and Blackrock jointly founded Greenlane to develop and operate a U.S. nationwide charging and hydrogen fueling network for commercial vehicles, while Europe’s largest truck manufacturers founded Milence to develop a similar commercial charging network in Europe.

Even traditional energy and utility companies, including BP, TotalEnergies, Iberdrola and Enel, have been active in developing charging networks, with each of these companies founding their own charging network joint ventures in the last two years alone.

© Ankura. All Rights Reserved.

If the world wants any hope of limiting global warming to a 1.5°C increase — as agreed to in the Paris Agreement — governments and the auto industry must work together to promote the widespread adoption of zero-emission vehicles. Governments are doing their part — more than 20 countries aim to phase out internal combustion engine car sales by 2050, while over 120 countries have announced economy-wide net-zero goals. For the auto industry to do its part and lower the EV cost curve, automakers must learn to use joint ventures and strategic partnerships effectively.

However, joint ventures and partnerships present their own set of challenges and risks. Potential partners need to negotiate key deal terms like scope, decision rights, and preemptive dispute resolution. [2]For more on joint venture deal making, see James Bamford, and David Ernst, “What’s the Best Way to Structure a Joint Venture?” The Joint Venture Alchemist, February 2023, … Continue reading Considering the evolving technological landscape, partners also need to consider how to safeguard their intellectual property. [3]For more on intellectual property issues unique to joint ventures, see Tracy Branding Pyle, and James Bamford, “Protecting IP in Today’s Joint Ventures and Partnerships” The Joint Venture … Continue reading And once the partnership is operational, there can be other challenges, like managing conflicts of interest among partners who are also competitors, managing competitively sensitive information, and aligning on strategy and financials. Many of these challenges can be handled with expert guidance on detailed business planning, well-drafted deal terms, and robust governance. While the EV transition is a daunting challenge for governments, companies, and consumers, joint ventures and partnerships — when structured and governed effectively — can help pave the way ahead.

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.

Comments