s End" loading="lazy" >

s End" loading="lazy" >

Managing Misalignment in Joint Ventures

JV agreements can be tailored to more effectively prevent, de-escalate, and resolve disputes.

FEBRUARY 2022 – In the last year, many high-profile joint ventures have come to an end. Uber exited three JVs in Russia and restructured a fourth to provide local partner Yandex with a clear path to full control. John Deere and Hitachi ended their 30-year joint venture to distribute construction equipment in the Americas. And Renault ended its joint venture in China with Dongfeng due to poor sales.

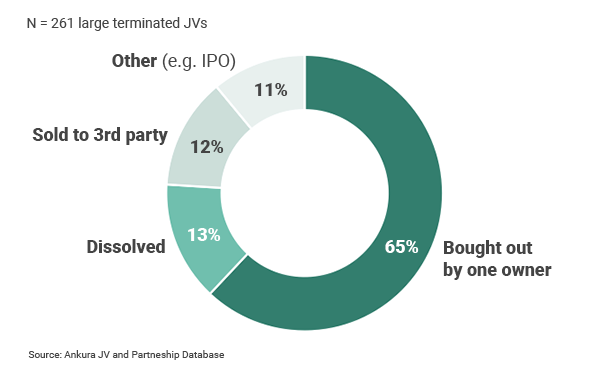

Such terminations should not be surprising. The median joint venture lasts 10 years – a figure that has remained largely unchanged for decades. While JVs in relationship-driven geographies such as Asia and the Middle East, as well as asset-style JVs in slow-twitch industries like oil and gas, mining, and chemicals often last twice as long, the fact remains that all joint ventures come to an end, often earlier than partners anticipate.

Stock markets are also paying attention to JV exits. In looking at how exiting a material joint venture impacts the share price of parent companies, we found that 54% of JV exit announcements had abnormal returns for at least one parent, with a median positive return of 5.0%. “Buying” partners tend to have higher abnormal share price returns than “selling” partners.

Getting exit right is essential to maximizing a company’s returns from a joint venture. In mountain climbing, more people are killed going down the mountain than going up. The same is true in joint venturing. Poorly structured exit provisions can cause significant time delays for companies to exit underperforming businesses, to monetize investments, or to execute broader strategic moves. Poorly structured exit provisions also can exacerbate partner animosity, trigger litigation, cause reputational damage, spawn high legal fees, and negatively impact exit valuations. All destroy shareholder value.

Given the importance of exit, we’ve been looking more closely at how companies structure exit terms in legal agreements. To do this, we’ve benchmarked the exit provisions of 81 joint venture agreements from around the world. Here’s a snapshot of what we found:

To read more about designing JV exit terms, please see our recent whitepaper on exit provisions:

Joint Venture Exits: Five Steps to Structuring Robust JV Exit Terms

To learn more about how Ankura advises clients on JV and partnership transactions, governance, restructurings, and exits, please contact James Bamford or Tracy Branding Pyle.

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.

Comments