s End" loading="lazy" >

s End" loading="lazy" >

[Infographic] Independent Perspectives Prove Effective in Resolving JV Disputes

98% of disputes that have been referred to a dispute review board do not proceed to arbitration or litigation.

The hidden logic for holistically structuring exit terms in joint ventures.

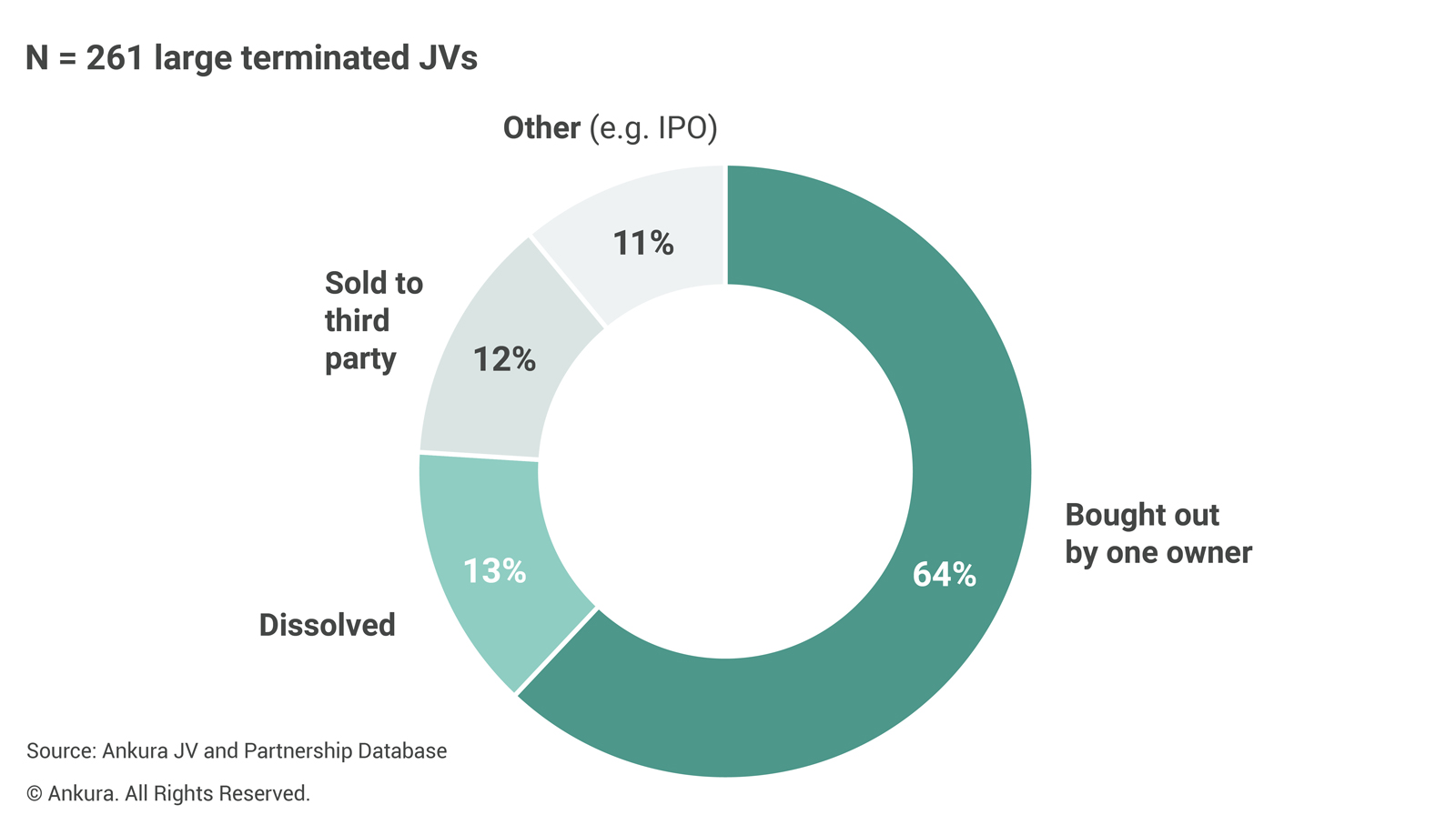

FEBRUARY 2022 — All joint ventures come to an end. The median lifespan of a joint venture is 10 years — a time frame that has remained largely unchanged for decades. Some 65% of JVs end with the venture being bought out by one partner (Exhibit 1). The other 35% end in other ways, such as being unwound, dissolved, sold to a third party, or taken public.

"*" indicates required fields

Because JVs are not permanent, potential partners must think through the terms of the inevitable separation. Unfortunately, exit negotiations are often pushed to the eleventh hour and not fully considered. Too often, potential partners do not have a clear view on the exit rights they want, what rights are reasonable to give their partner, and how these rights will play out under different future scenarios.

This white paper will shed some light on how companies should address exit terms in joint venture negotiations. Specifically, we outline the costs of getting exit wrong, explain why exit terms are difficult to structure, and walk through a five-step process for defining an approach to exit in JV agreements. Our perspectives draw on benchmarking data on the exit provisions in 81 JV agreements and our experience structuring and restructuring hundreds of JVs. This paper is part of an ongoing series on JV dealmaking intended to bring structure, data, and perspectives to negotiating and structuring JV legal agreements.[1]For additional discussion on at-will exits, please see the 2022 Ankura White Paper: At-Will Exits in JV Agreements: Eject Buttons Often Come with Strings Attached, by Edgar Elliott, Tracy … Continue reading

Getting exit terms wrong in joint ventures can be costly. Poorly structured exit provisions can cause significant time delays — to get out of an underperforming or non-strategic business, to monetize initial investments and access trapped capital and other assets, or to execute broader strategic moves. Poorly structured exit provisions can also exacerbate partner animosity, trigger litigation, cause reputational damage, spawn high legal fees, and negatively impact exit prices. All destroy shareholder value.

Many JV exits illustrate these costs. Consider a 50:50 media JV in India between a global player and a local firm. The agreements committed each partner to use the JV as its exclusive vehicle in India for certain high-growth broadcast and streaming-related services. The business was underperforming in the fast-growing market and needed investment to maintain market share, let alone grow relative to competitors. However, the Indian partner was unable to invest, was unwilling to take on debt, and did not approve investments proposed by the partner or management team. The global firm made a fair offer to buy out its partner, but this offer was rejected. Perhaps the Indian partner realized the value to the global partner of owning the JV outright was greater than that implied by an external “fair market” valuation – a situation not uncommon for savvy partners to realize. In the end, the global partner paid a price 40% above fair market value to buy out its partner and regain its freedom to operate in India, a key growth market.

Or consider Fuji Xerox, a multibillion-dollar joint venture between Xerox and Fuji Photo Film, founded in the 1960s as a way for Xerox to access the Japanese market. In a complicated turn of events, when Xerox was in financial distress in the last decade, its potential attractiveness to a third-party buyer was impeded by exit terms in its Fuji Xerox joint venture. Specifically, the Fuji Xerox venture agreements provided that if Xerox was acquired by a third party, Xerox lost certain governance rights in the JV as well as the right to use critical intellectual property and trademarks in Asia for multiple years. This led Xerox to eventually agree to be bought by Fuji as other buyers were less interested in purchasing Xerox given its intellectual property in the Asia-Pacific market was tied up in the JV. Activist investors filed suit, and eventually Xerox terminated the merger agreement, which in turn led to Fuji filing suit against Xerox regarding such termination. Fuji and Xerox then negotiated a separate exit for Fuji Xerox under which Xerox sold its stake in the JV to a Fuji subsidiary. This debacle involved lengthy and expensive litigation among JV partners and shareholders that destroyed significant value.

Structuring robust exit provisions in joint ventures is challenging for all sorts of reasons. This is not just because partners often wait to discuss these terms until late in the game when there is pressure to sign the deal, though that certainly can be a contributing factor. It is also not simply because partners are excited about the momentum of the deal and do not want to detract from the romantic view of a new partnership with a potentially contentious debate about a future divorce, though this, too, can play a role.

It is also challenging because JV exit terms are inherently complex. Such terms are spread across many parts of the JV agreement, often appearing in sections related to transfer of interests, termination, breach of agreement, covenants, other provisions, and even in commercial agreements outside the shareholders’ agreement. Similarly, for senior executives and other non-lawyers, the combination of exit triggers, exit mechanisms, and potential valuation approaches may seem almost limitless. This can make exit terms hard to track and view holistically. The challenges multiply, and potential options proliferate, when a potential JV has more than two partners.

Adding to the challenge is uncertainty about the market or technology. JVs are often used in frontier businesses — i.e., new technology domains, new market segments, and new countries — for which the future is much harder for firms to predict than in core existing operations in which mergers and acquisitions (M&As) and organic investments tend to be favored. This makes it difficult to know when, why, or by whom an exit may be needed, and difficult to know what exit provisions will benefit or harm a particular partner.

In sum, structuring joint venture exit terms is complicated — and it requires strategic thinking that combines business and legal skills. But it is not five-dimensional chess. There is a way to think about exit in a structured way that allows dealmakers and lawyers to engage jointly, fully, and thoughtfully in shaping exit principles and contractual terms, and paving the way for smooth off-ramps in joint ventures.

A five-step process can help organize and simplify the thinking on JV exit terms (Exhibit 2). These five steps are: (1) review strategic considerations affecting exit, (2) define exit triggers, (3) determine the best exit mechanisms for each trigger, (4) define valuation approaches, and (5) address post-exit needs. Each step is detailed below.

Step 1

Review Strategic Considerations Affecting Exit

Step 2

Define Exit Triggers

Step 3

Determine Which Exit Mechanisms Are Best For Each Trigger

Step 4

Define Valuation Approaches

Step 5

Address Post-Exit Needs

Source: Ankura

© Ankura. All Rights Reserved.

Before drafting or responding to contractual terms, a company considering a joint venture should internally align on the strategic context affecting exit. We have found it quite useful to conduct a structured working session — ideally with participation from the business sponsor, corporate strategy and business development team members, and attorneys — to talk through a set of questions that shape what exit terms to include in a joint venture agreement.

One question to discuss: What is the desired end game of the venture? For instance, is the JV intended as a long-term partnership, a staged exit for the company or its partner, a path to bring in additional partners, or a stepping-stone to an initial public offering (IPO)? For example, when Russian ride-hailing tech giant Yandex and U.S.-based Uber restructured the ownership of their ride-hailing JV in Russia, the parties knew that Yandex might wish to buy out 100% of the venture in the near future and included a call option for Yandex to buy out Uber at a predetermined price. What are other end-game scenarios, including potential bad outcomes for the company? How likely are these and what might cause such endings?

A related question: Who is the “natural buyer” or the “natural seller” of the JV? In our experience, one partner is likely to be better positioned to buy out the JV — for instance, if the venture is co-located on its site, is more core to its business, or receives critical technology or services from that partner. For example, a chemical manufacturing JV between Sumitomo and Trinseo was located on and integrated with a Sumitomo-owned site and other chemical assets. This made Sumitomo the natural buyer of the JV. Not surprisingly, Trinseo ultimately sold its interests to Sumitomo.

Financial and regulatory considerations also impact the natural buyer-seller calculus. For instance, it is worth asking: What are the likely additional capital needs of the JV, and is one partner financially stronger than the other and better able to fund future investments, losses, or a buyout? Similarly, are there any regulations, licenses, financing agreements, permits, or other agreements that may impact a partner’s ability to exit? Some financing agreements require a guaranty from one or more partners. If a guarantor exits the JV, a failure to secure an acceptable replacement could put the venture in breach of its financing agreement and constrain how a partner might be able to exit. Or regulations could require certain ownership structures, such as majority local ownership, which could prevent one partner from taking over the JV. Similarly, time limitations of certain government permits or licenses might provide a natural duration for the JV, after which the parties will be required to renew the agreements.

Other questions relate to negotiating power. Companies would be wise to ask: Do we have more leverage now versus later, and how might that affect our negotiating stance on exit terms? For instance, a local company entering into a JV with a global firm might have more leverage in the future, once it has developed capabilities and learned the business through the JV. This might push the local firm to be silent on certain exit terms and use its leverage when it is in a stronger position.

Other questions provide more tactical guidance to the negotiating team. For instance: Does the JV need time to get off the ground, and would it benefit from a “lock-up” period during which no partner can exit? Similarly, what commercial commitments and transition service agreements, such as the ongoing provision of support services, technology licenses, supply or purchase agreements, and land use rights, will need to be in place post-exit and for how long? Working answers to these and other questions set the stage and context for structuring exit terms.

Having talked through the strategic context for exit, it is time to shape specific contractual terms. This starts with defining what events should allow one or more parties to exit the venture. Our review of joint venture agreements identified 16 categories[2]An exit category may include more than one distinct triggering event. For example, a breach of the competition provisions in the JV agreement could be one possible trigger, material breach of the JV … Continue reading of possible exit triggers (Exhibit 3). Most JV agreements contain four to eight categories of triggers, though some have far more individual triggers. For instance, the legal agreement for BMW’s joint venture in China with Brilliance Auto Group contains 22 specific triggering events across 11 of the categories. The full list of exit triggers can serve as a checklist for the deal team to identify what types of events might create the option for a partner to exit.

| Relevant? | |

| Partner Breach or Default | |

| Partner Bankruptcy or Insolvency | |

| Partner Change of Control | |

| Partner Deadlock or Dispute | |

| Partner or JV Becomes Subject to Sanctions | |

| Partner Ownership Falls Below [•]% | |

| JV Performance — Negative, Milestone Missed1 | |

| JV Performance — Positive, Milestone Achieved | |

| Partner Underperformance2 | |

| Partner or JV Fails to Obtain Required Consents or Permits | |

| Partner or JV License or Trademark Expires or is Cancelled | |

| Partner Supply or Purchase Agreement Expires or is Cancelled | |

| Material Change in Laws or Regulations | |

| Force Majeure / Catastrophic Event | |

| JV Term Expires | |

| Other3 | |

| 1 Examples include: (i) missed revenue or profitability targets; (ii) missed technology or product milestones; (iii) failure to meet business ethics, human rights, environmental, or other agreed performance standards; and (iv) JV insolvency or bankruptcy. 2 Examples include: (i) failure of partner technology to meet performance guarantee; and (ii) partner (as operator) to meet agreed performance standards. 3 Examples include the partner loss of right to appoint board directors, chief executive, or other officers of the JV due to changes in laws or other reasons. Source: Ankura © Ankura. All Rights Reserved. |

|

|---|---|

© Ankura. All Rights Reserved.

For example, a right to exit the JV may be triggered by another partner breaching the JV agreement by making a false representation or warranty, filing for bankruptcy, becoming subject to sanctions, or undergoing a corporate change of control. Similarly, exit might be triggered when the partners are deadlocked on a highly material decision.[3]In a broader analysis on dispute mechanisms, we found that partner dispute is a defined exit trigger in 25% of JV agreements. When such provisions exist, they are ideally limited to a few highly … Continue reading Furthermore, a partner’s ownership falling below a certain threshold (e.g., 10%) — perhaps due to non-participation in capital calls and subsequent dilution — may trigger a right for other partners to buy out that partner. The rationale: A small minority shareholder can impose a heavy “governance tax” on the venture and its partners through its ability to conduct audits, request information, and, depending on the voting passmarks, block decisions.

Other triggers could relate to the JV performance or prospects of the JV business. The right to exit the JV could be triggered if the JV fails to secure a material regulatory license or falls short of a minimum level of sales or profitability within a defined period of time. For instance, in a multibillion-dollar JV between Goodyear and Sumitomo, the agreements established if the venture did not achieve a 6% share of the tire market in Japan, either partner had the right to initiate exit. Conversely, exceptional venture performance may also trigger exit rights, especially for a minority non-controlling partner. In certain circumstances, it may be appropriate if the venture has achieved profitability or valuation targets within a given time window (e.g., between years three to five) for a partner to have the right to initiate a process to sell shares to the public through an IPO.

Not all JV exit rights are triggered by events. In many instances, one or more of the parties may wish to have the right to exit “at will” (i.e., simply because it wants to). We saw such at-will exit rights in 60% of JV agreements we analyzed. Of the venture agreements that contain an at-will exit right for one or more partners, almost all agreements — 98% of agreements reviewed — place some restrictions on this right to exit. Restrictions include the right of the non-exiting partners to intervene, such as by exercising a right of first refusal (ROFR) or a right of first offer (ROFO). Such restrictions may also relate to limitations on when, how, or to whom interests can be transferred (e.g., only after a lockup period if 100% of the partner’s interest is transferred or if the transferee has certain characteristics).

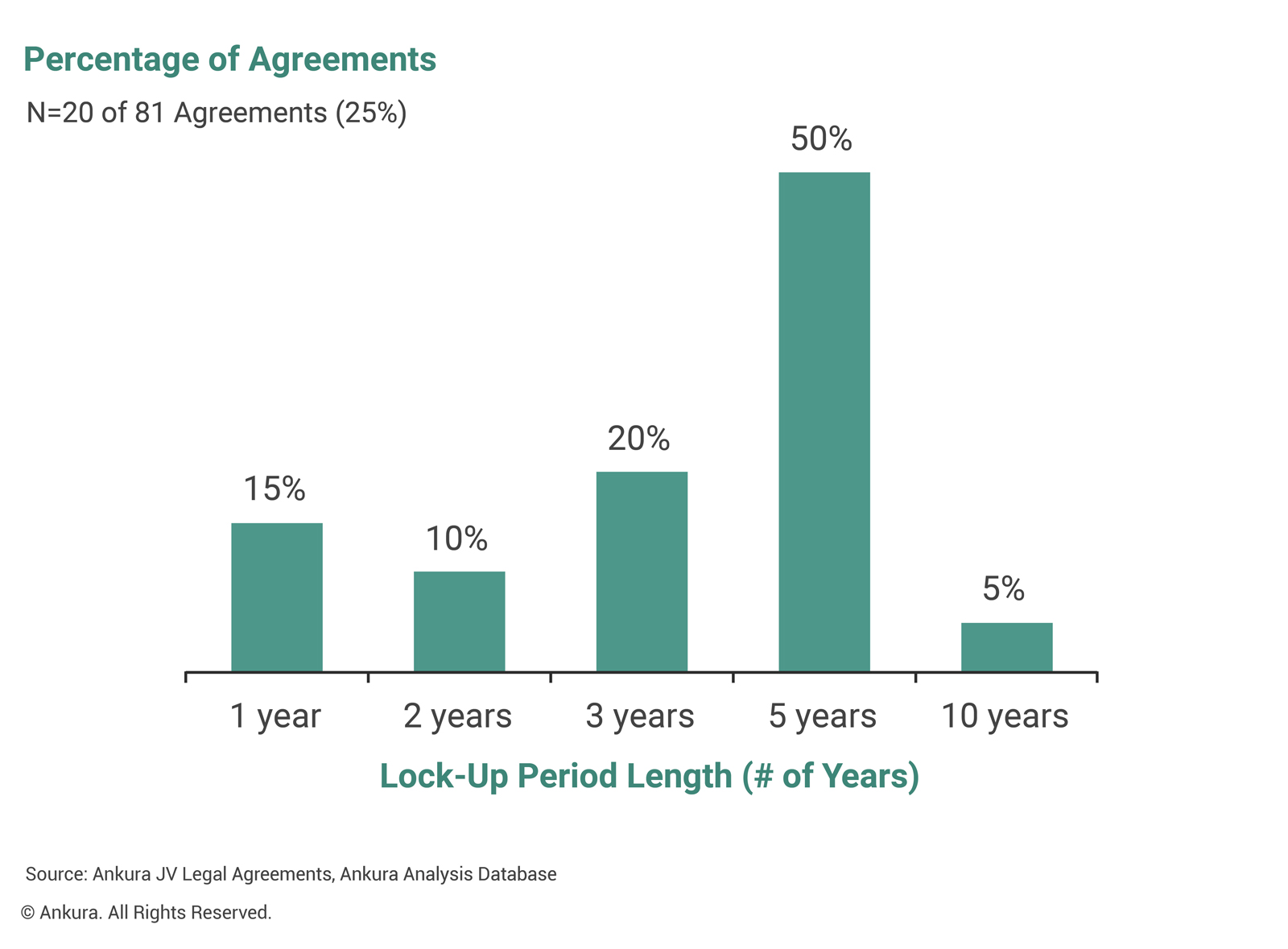

A final point to consider regarding exit triggers is when triggers should be available. Should certain exit triggers, like the right to exit at will, be off limits while the JV gets up and going? If so, the parties should consider a lock-up period during which partners cannot exit the JV. A quarter of joint venture agreements have a lock-up period. The length of the lock-up ranges, with five years being the most prevalent (Exhibit 4).

© Ankura. All Rights Reserved.

Also, should certain exit rights — such as those linked to positive or negative performance — expire after a period of time? For example, in a biofuels JV, the agreements included a right for either partner to exit if the venture failed to deliver at least $15M in annual profits in any of the first five years. That exit right no longer applied after year five.

For each identified exit trigger, the parties will need to determine the appropriate exit mechanism. For instance, will a given trigger provide one or more partners the option to sell its ownership interests to a third party, to “put” its interests to the other partner, to buy out the other partner, dissolve the venture, or initiate an IPO process? Similarly, does the non-initiating party have any rights, such as a right of first refusal or right to tag along, in an exit?

Potential exit mechanisms vary significantly based on the triggering event and venture context. In simple terms, exit mechanisms can be broken down into rights for the party triggering the exit and rights for the non-triggering party (Exhibit 5).

| Rights of the Triggering Party |

|---|

|

|

|

|

|

|

| Rights of the Non-Triggering Party |

|---|

|

|

|

|

© Ankura. All Rights Reserved.

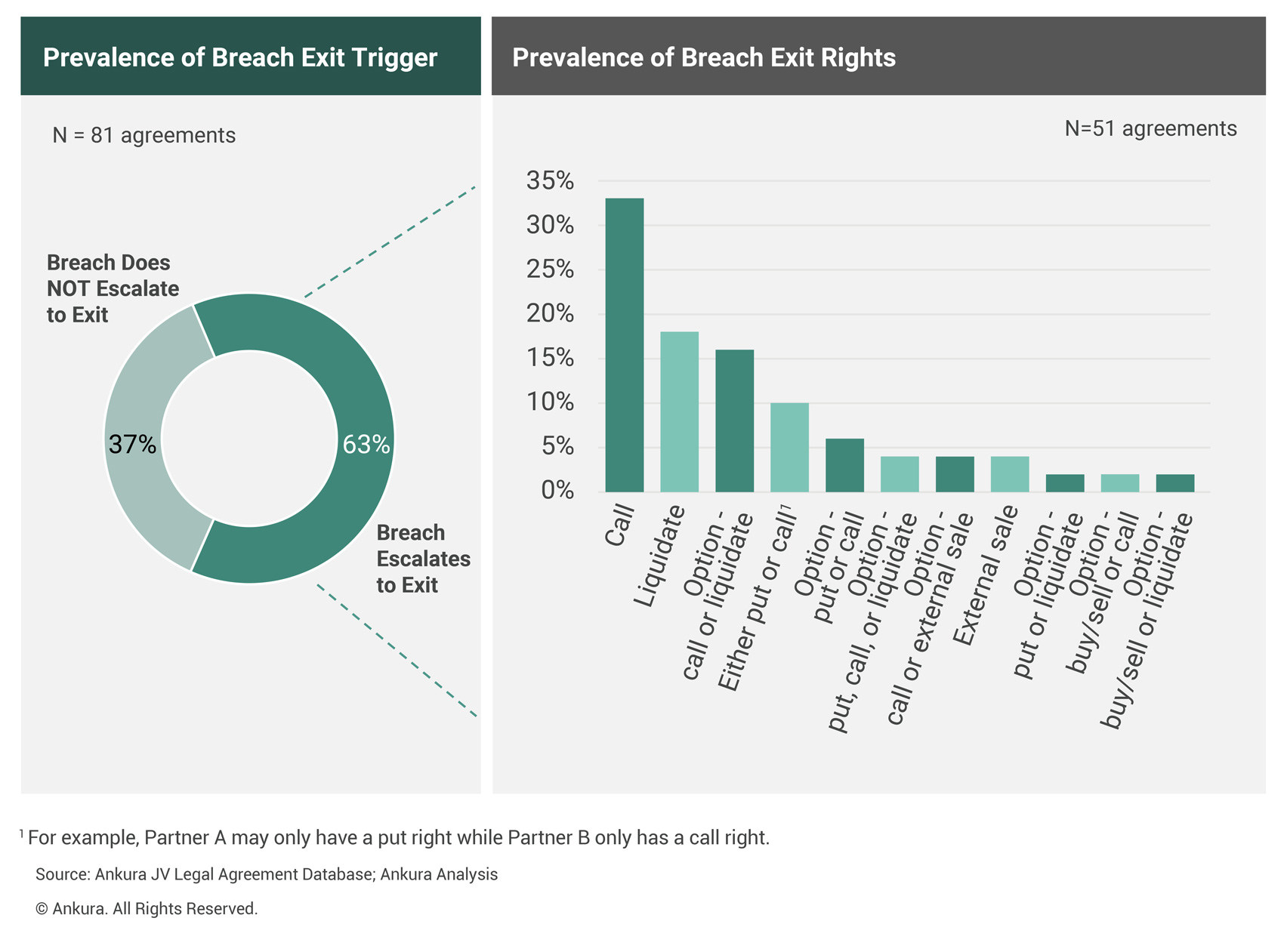

Certain exit mechanisms tend to be used in at-fault situations, while others are more often used when no one is at fault, and a partner wishes to leave the venture at will. Consider one at-fault situation: When a partner is in material breach of the joint venture agreement, and the breach has not been cured, the breach gives the non-breaching partner the right to exit. Our analysis shows that roughly two-thirds of venture agreements include uncured partner breach as an exit trigger. Among the agreements reviewed, 11 different exit mechanisms are used (Exhibit 6). The most common is to provide the non-breaching partner the right to call the breaching partner’s shares. Other common exit mechanisms include liquidation (18% of agreements in which partner breach is a trigger), and a right to choose between calling the breaching partner’s shares or liquidating the venture (16% of agreements in which partner breach is a trigger). Puts, calls, and liquidation are also common mechanisms in at-fault scenarios such as in the case of partner breach.

© Ankura. All Rights Reserved.

By contrast, puts, calls, and liquidation rights are rare when a partner is exiting simply at will. In such cases, a ROFR or ROFO for the party not triggering the exit are common. This is because in an “at-will” exit scenario, the exiting partner typically can transfer interests to a third party subject to restrictions: 33% of agreements place restrictions on the identity of the transferee and a majority of agreements give the non-exiting party a ROFR or ROFO.

Some exit mechanisms are more common when the exit trigger requires a partner to be at fault than when the trigger is a partner leaving the venture at will. Other exit mechanisms are more common for minority partners, while still others are more prevalent among majority owners. A partner with a smaller minority interest is more likely to have a tag-along right — the right to force the purchaser of its partner’s interests to also purchase its interests — so it can capitalize on a sale by a larger majority partner. By contrast, the majority partner is more likely to have a drag-along right, which is the right to force your partner to sell its interests to a third-party buyer when you sell to such buyer. This drag-along right enables sellers to give a buyer the option of owning 100% of the JV company. Similarly, a minority partner is more likely to have a put right than a call right. After all, it is more likely a large majority owner would be willing and able to purchase a small minority partner’s interest on demand than a small minority partner (who may be more cash constrained) would be willing and able to purchase a large majority partner’s interest on demand.

Parties should select an appropriate exit mechanism for each exit trigger based on the nature of the trigger, the partners’ ownership in the venture, and the partners’ broader interests and constraints.

Certain exit mechanisms require the partners to agree on a valuation for the interests in the JV that are being transferred. For example, if a partner has a right to call a breaching partner’s interests, at what price can it call these interests and under what payment terms? Partners should predetermine how interests will be valued in such scenarios. More broadly, in most exits or transfers of interests, the interests of the exiting partner need to be assigned a value.

There are numerous options for how the partners could determine an appropriate price. Four common approaches are:

Partners should also consider whether there should be caps on the value of the interests above which a partner is not forced to buy or a floor on the value below which a partner cannot be forced to sell. Caps and floors can limit unforeseen variability and make the potential for an exit more palatable in negotiations.

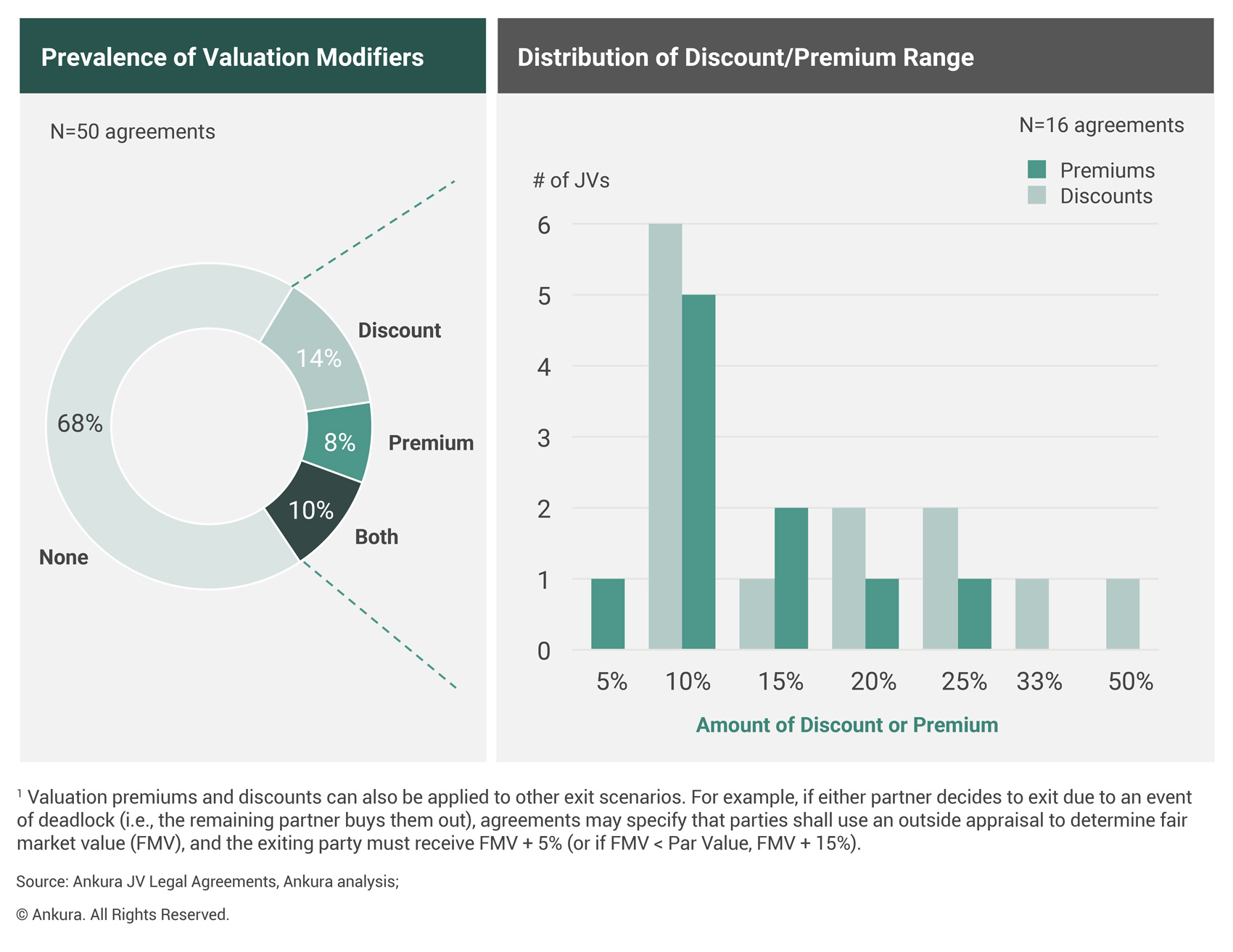

A final consideration is whether there should be a discount or premium on the value of the JV interests, particularly if a party is at fault. If a party breached the JV agreement or is otherwise at fault and must sell its interests, does it do so at a discount as a penalty? Or, if it must purchase its partner’s interests, must it purchase them at a premium? Our analysis found that 32% of JV agreements included a premium, discount, or both in the event a party is at fault. Specifically, 14% of agreements required a sale at a discount, 8% of agreements required a purchase at a premium, and 10% of agreements mentioned both a discount and a premium, depending on the circumstances. The most common amount of this premium or discount was 10% (Exhibit 7). In addition to being used when a party is at fault, discounts can be used to disincentivize an early exit from the venture. For example, when Clorox and Procter & Gamble created a food container joint venture under the Glad brand name, the agreement was structured so that a party exercising a put right would receive a lower amount early in the life of the venture, thus disincentivizing them to exit.

© Ankura. All Rights Reserved.

Last, but certainly not least, is determining what ongoing relationships could or should exist between the JV and exiting partner following the exit. JV partners should consider a number of key questions.

Answering these questions is sometimes challenging. For instance, Airbus and Saudi Arabia Military Industries (SAMI) recently announced a joint venture for the maintenance, repair, and overhaul of military aircraft in the Kingdom of Saudi Arabia. If Airbus exits the JV, the JV will potentially be missing critical know-how. If SAMI exits the JV in the future, the JV may struggle to obtain business from the Saudi military. Thus, post-exit arrangements in such a scenario would be challenging and likely require some commitment from each party to support the JV — either by staying in the JV or by supporting the JV even if the partner exits in the future.

Knowing your joint venture will end, are you including exit terms in your JV agreement that set you up for a smooth exit? While negotiating exit terms can be challenging, methodically following this five-step process can help you thoughtfully approach exit and include terms that will facilitate future changes in JV ownership. Do not wait — plan for the end at the beginning.

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.