[Infographic] Independent Perspectives Prove Effective in Resolving JV Disputes

98% of disputes that have been referred to a dispute review board do not proceed to arbitration or litigation.

Recent benchmarking of renewable energy and chemical companies

November 2021 – We recently benchmarked the corporate development functions of 24 companies across the renewable energy and chemicals industries. Our goal was to understand how firms organize corporate and business development to execute M&A, JV, investments, and partnership transactions, and to give some dimensions to their deal funnels and close rates.

Key findings from our research include:

© Ankura. All Rights Reserved.

© Ankura. All Rights Reserved.

These numbers are directionally consistent with what we have seen in other asset-heavy sectors, including mining and industrials, as well as more technology-driven sectors, such as pharmaceuticals and high-tech.

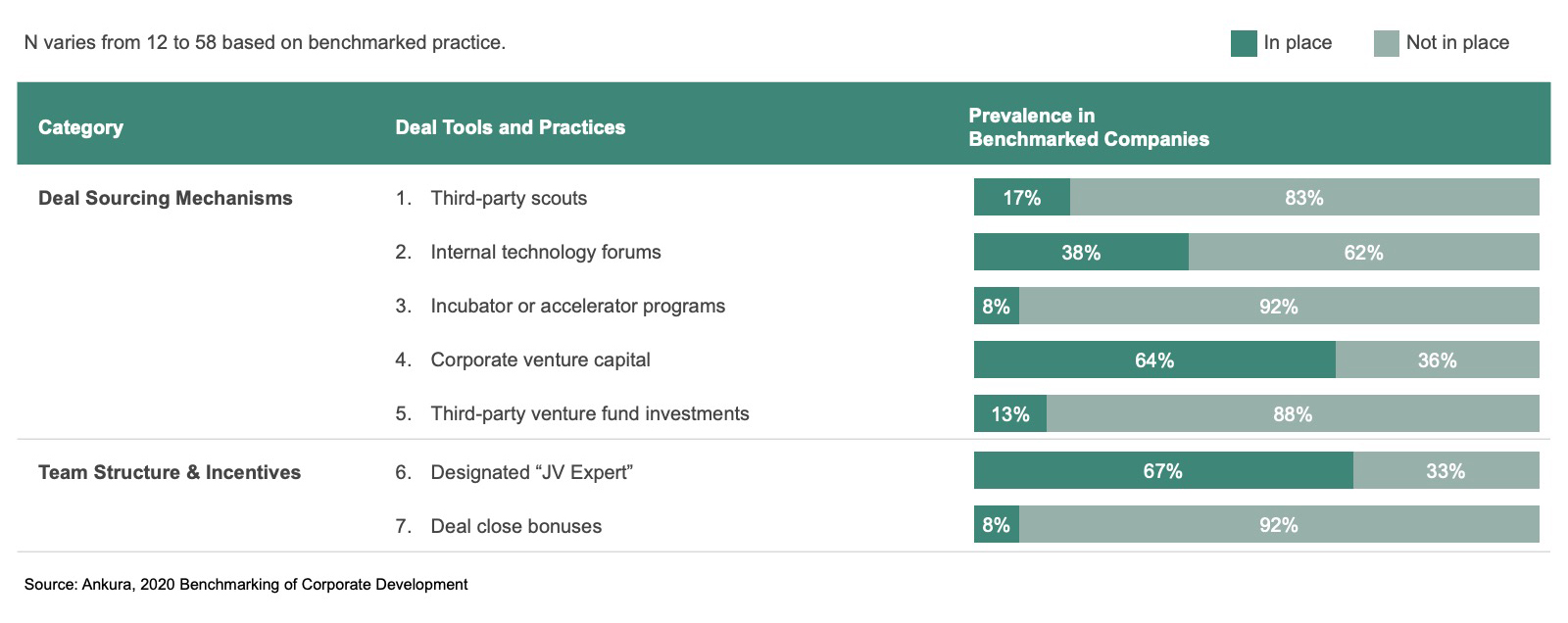

Companies are also rethinking the processes and tools they have to support corporate development – especially in light of the uptick in technology- and sustainability-related JVs, minority investments, and non-equity partnerships. We have benchmarked these processes across several industries (Exhibit 3). Our dataset includes the same 24 renewable energy and chemicals companies from Exhibit 1, plus an additional 34 companies in the oil and gas and mining sectors.

© Ankura. All Rights Reserved.

We found that nearly half (47%) of companies have revised their investment stage gate process to explicitly accommodate JVs and non-equity partnerships, including clarifying different decision thresholds, approvers, and input requirements for each gate based on certain transaction types. For instance, a deal lead managing a potential JV transaction through an internal review might be expected to provide an analysis of the counterparty’s partnership history, frame alternative venture structures including different scope, ownership, and control combinations, and a lay out a vision for potential evolution and end-game scenarios. These issues are highly relevant to evaluating a potential JV transaction, but much less so in an M&A deal.

Similarly, 43% of companies have developed a JV Major Clause Guide – that is, corporate guidance establishing minimum and preferred language across key provisions and terms in JV agreements. The purpose of such a document is to ensure that new JV agreements address key risks and reflect prior learnings and best practice.[4]See Tracy Branding and James Bamford, “No Clause for Concern: Developing a Major Clauses Guide for Better JV Transaction Structuring,” The Joint Venture Exchange, April 2019. And 29% of companies have explicitly included lookbacks as a final gate at the conclusion of their deal process to identify lessons learned for future deals, and drive them backwards into their JV-related terms and processes.

Reflecting on our conversations and looking to the future, the next frontier of corporate development functions is likely to include improvements in four areas:

Today, corporate development organizations are taking a more strategic and broader role in many companies – and screening, negotiating, and structuring a more diverse set of transaction. As we would expect, we are seeing that the teams, processes, and tools to support Corporate Development Officers are also evolving within, albeit with mixed pace across firms.

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.

Comments