Board Ballet: Choreographing the JV Board Agenda

An annual agenda that balances operational reviews with discussions of strategy and growth will help JV Boards be as effective as possible.

Who needs to approve this? It’s a question commonly asked by corporate executives. But in joint ventures, it’s not that simple.

SEPTEMBER 2022 — Who needs to approve this? It’s a question commonly asked by corporate executives. Usually, getting the answer is straightforward. Executives rely on their past experience, ask colleagues, or consult the company’s delegation of authority (DOA) policy or other organizational documents, and they have their answer.

But in joint ventures, it’s not that simple.

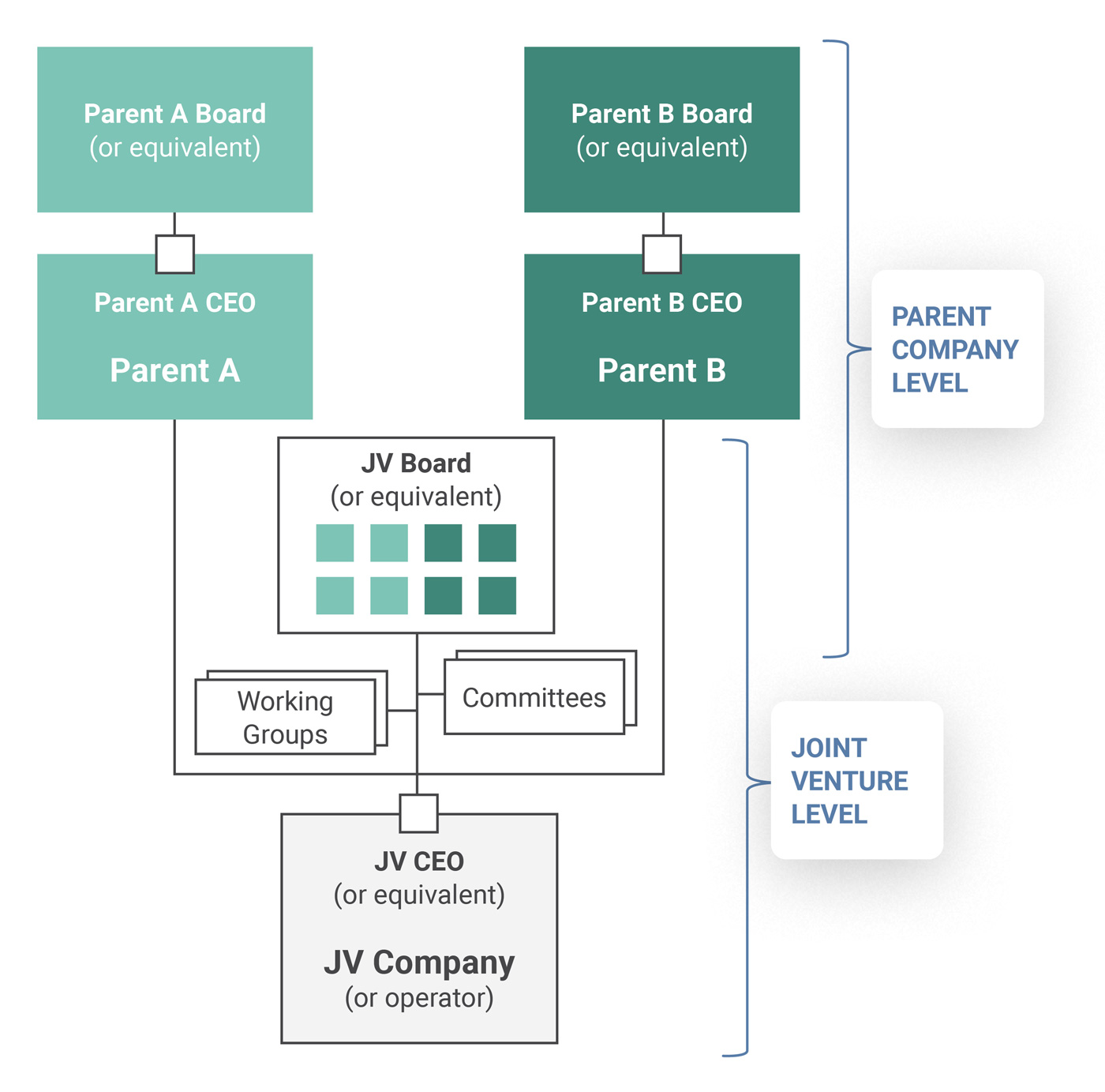

For starters, that’s because the question needs to be answered at two levels (Exhibit 1). First is at the joint venture. Consider any major decision in a JV – a proposed plan and budget, individual expenditure, third party contract, organizational restructuring, or any other decision. Does JV management have the authority to make that decision, or does it require the review or approval of a Board committee, the full Board, or the shareholders?

© Ankura. All Rights Reserved.

Second is at the parent company. For a committee member, Board Director, or shareholder representative to “vote” on a matter, do they need to secure input or pre-approval from others within their company? For instance, does the JV’s proposed dividend distribution or new line of credit first require sign-off from the parent finance organization? Similarly, do other decisions require sign-off from the parent company’s human resources, legal, procurement, or other function?

The presence of these two levels is not the only complicating factor. In JVs, there are almost always numerous documents, including parent company DOA policies, JV legal agreements, and Board and committee charters, that lay out authorities. These documents may be incomplete, include different delegation line items, have different monetary thresholds, or contradict each other in other ways. Changing delegations – say, to fix inconsistencies or to reflect the JV’s maturity – often requires re-opening core legal agreements, something that partners are often reluctant to do.

What’s more, JVs lack certain cultural advantages of wholly-owned companies. For example, in a wholly-owned context, everyone is ultimately working for the same firm. People may have many shared experiences and touchpoints, and an expectation to be working together for a long period of time. This aligns interests and creates common norms. It also enables individuals to make decisions without always first clarifying or securing needed approvals (the “ask for forgiveness later” strategy).

In JVs, none of this may be true.

JV Board Directors and committee members may have never worked in a JV before and regularly turn over after just two or three years.[1]See “Public Company vs. JV Governance,” James Bamford, Tracy Branding Pyle, and Lois D’Costa Fernandes, Harvard Law School Forum on Corporate Governance, December 28, 2019 (showing median board … Continue reading JV management teams may be composed of secondees from different parents who have different loyalties. These circumstances make it hard to build strong personal relationships and to understand the rhythm of consensus-building and decision-making. They also depend on informal working norms. Additionally, JV Board Directors almost always have fiduciary duties to the venture, which make it hard for them to know where they can vote based on their own independent judgment versus when they must defer to guidance from their shareholders.

These added challenges give rise to two types of pitfalls in JVs – overly loose and overly tight delegations. History is replete with JVs falling into one of these ditches:

Poorly defined delegations can lead to rogue, under-supervised decisions. For example, in a large industrial JV in the Middle East, the Directors from one parent approved the JV taking out a third-party loan without first vetting the decision with the finance and legal teams in the parent. The result: The loan tripped the parent company’s covenants in its own financing agreements, causing it to be in default. In another JV with that same parent company, the JV CEO reduced the amount of health, safety, and environmental (HSE) and maintenance training provided to staff without consulting the Board. Eighteen months later, the JV started to experience a performance drop and an uptick in HSE incidents – with the Board not discovering the cause until after a shareholder audit.

In other instances, byzantine input requirements and a bias to over-inclusiveness can slow decision-making to a near halt. For example, in a large Canadian natural resources JV, one shareholder required all JV decisions to have the approval of a very senior executive. That executive was not on the Board, only had a few hours every month to dedicate to the JV, and almost always required the JV Directors to seek additional information from the JV after being presented with a decision for approval. This led to that shareholder requiring multiple months to approve any decision. This delay caused the JV to miss a deadline to lock in discounted third-party technology licensing fees that expired before the JV could obtain Board approval.

Many JVs fall into one of these ditches – and some JVs careen from one side of the road to the other, falling into both.

At Ankura, we help clients navigate and simplify this complex web of authorities and decision-making, working with individual JVs and parent companies with portfolios of JVs.

When we work with individual JVs on delegations of authority, we focus on answering three questions:

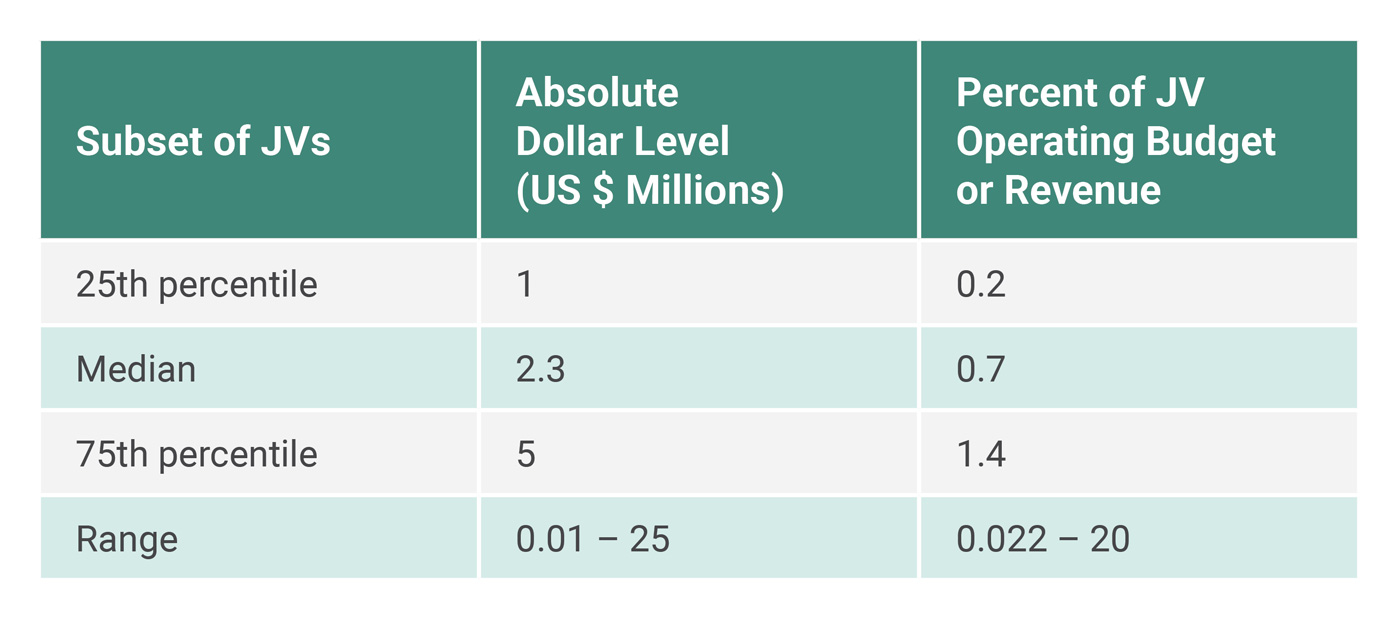

Are the agreed delegations still appropriate given the maturity of the venture? Delegations to JV management are, in most cases, quite low – often less than 1% of the JV’s operating budget (Exhibit 2).

© Ankura. All Rights Reserved.

This may make sense early in the JV’s life, when the parents want significant oversight as they build understanding of the business and trust in each other and the management team. But problems arise when companies do not revisit these low initial authority levels. For example, the CEO of a large LNG joint venture that had a billion-dollar annual budget only had the authority to sign off on expenditures up to $200,000. This meant the CEO was continually turning to the Board to approve contracts that were immaterial to the JV overall.

To address these issues, JV Boards should consider regularly reviewing and updating management delegations and increasing delegations to management, particularly to be at least 1% of the JV’s annual operating budget. As part of this process, we benchmark the JV’s delegations against the delegation levels in peer JVs to help JV Boards and CEOs calibrate delegations not just internally, but against the market.

Are there gaps or inconsistencies in formal delegations? A DOA policy, the JV Agreement, and other documents laying out authorities will inevitably not list every decision that will emerge in a joint venture, which can cause confusion and highlight different views among partners or JV management on who should decide what. Fortunately, there are actions JV partners can take to mitigate this issue. First is to ensure the thresholds and line items in the JV DOA policy align with delegations in other JV documents like the JV Agreement, bylaws, and/or articles of association – and vice versa. For example, if the JV Agreement states that the Board must approve material contracts over $10 million, the DOA policy should give the CEO authority to approve material contracts up to $10 million.

Second is to review the line items in the JV DOA policy, JV Agreement, and other documents outlining authorities against each parent company’s DOA policy to identify missing line items that may need to be added.

Third is to set a clear default rule about who makes decisions that are not listed in the JV DOA policy, JV Agreement, and other documents outlining authorities. In some JVs, such unlisted items are deemed to be delegated to JV management, while in others the Board must review all decisions not explicitly delegated to management. Either of these approaches can work. However, silence – not defining how unlisted matters should be decided – can be deadly.

Are shareholders sticking to an aligned-on approach to delegations? An owner of a Brazilian joint venture was concerned about the JV’s performance. In response, the owner convinced its partner to set up seven committees and eight working groups. In addition, the shareholder staffed a team of over 20 individuals to oversee the JV. While well-intentioned, these actions frayed relationships with JV management, who felt it had no authority to make decisions without shareholder involvement, despite having some authority per the JV’s DOA policy. Relationships with the other owner were also tense, as the other owner had neither the interest nor resources to be as involved in the JV. Ultimately, the problem – which is not unique to this JV – boils down to the fact that the partners and management were not aligned on an appropriate level of authority for JV management, despite what was clearly written in JV documents.

When this happens, JV stakeholders need to pause, come together, and align on expectations across the board. This may involve externally facilitated Board discussions to identify and bridge differences of opinion. Or it could involve developing procedures for sharing information between the JV and shareholders to avoid lopsided or ad hoc information sharing that can be detrimental to trust and also tax JV management who spend significant time responding to shareholder requests. Thus, JV partners need to align on an approach and stick to it, though this may be easier said than done given the number of stakeholders and interests in a JV.

When we advise parent companies about corporate policies and approaches for delegations across their portfolio of JVs and subsidiaries, we focus on three questions:

In our experience, the first step in the solution is to develop a corporate delegation guideline for JVs. This guidance document might apply to all JVs or be limited to a major class of JVs (e.g., non-controlled joint ventures). It might be an appendix to the corporate DOA policy or a separate document. And it might provide specific delegated authorities or only offer a common framework and leave the specific delegations to be determined for each JV separately.

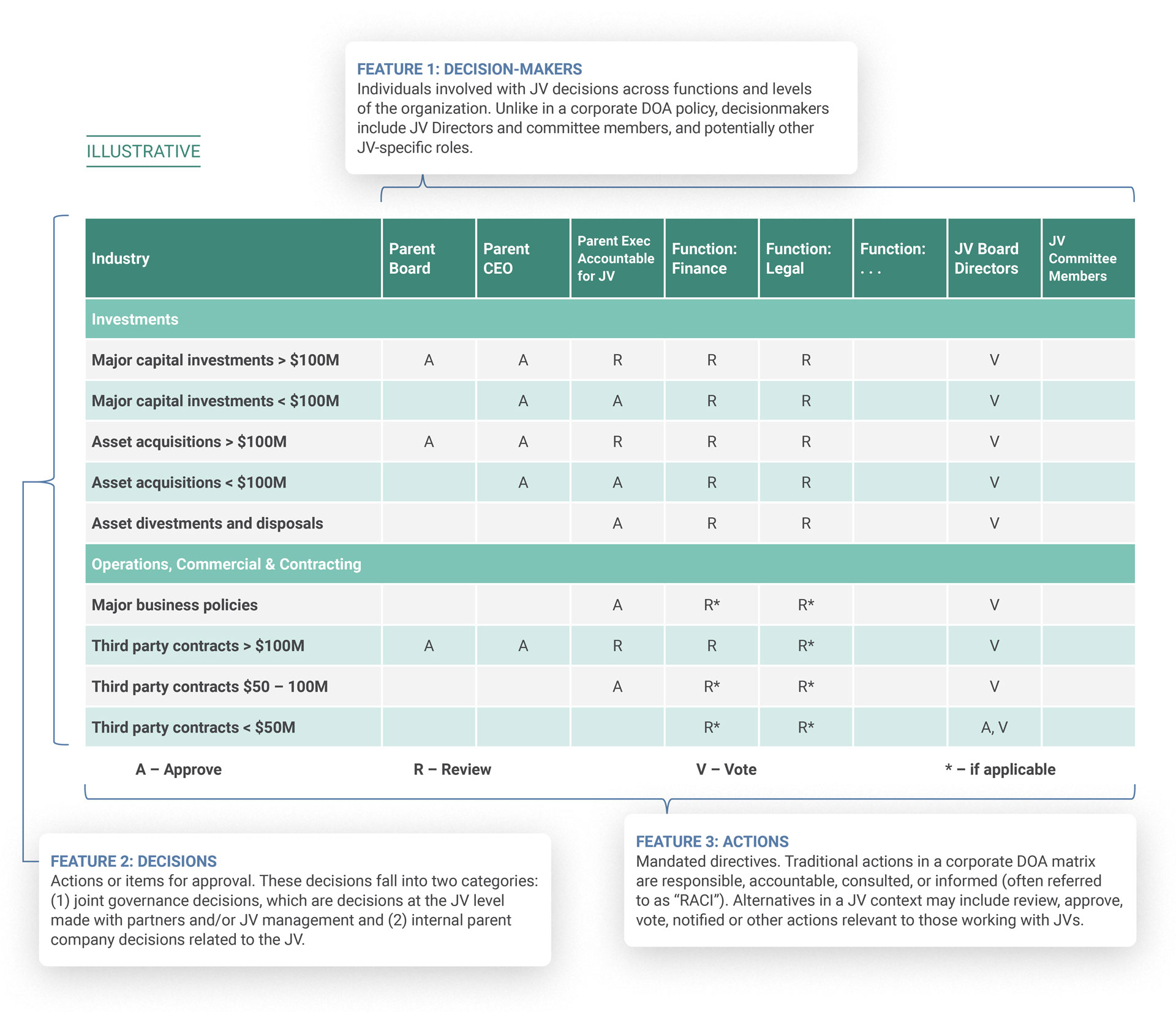

Irrespective of the scope, at the heart of this document is a delegations of authority table that maps with decision makers, decisions, and the nature of their roles (Exhibit 3).

© Ankura. All Rights Reserved.

The guideline should include additional guidance on when and how to apply the table. For instance, are monetary thresholds calculated based on the amount the JV is seeking to expend or your company’s percent interest of that amount? Do Directors need to obtain approvals any time they vote on a JV matter or only when that vote is or may be dispositive (i.e., the majority partner cannot decide on its own)? How should Directors address situations in which they believe the parent company’s guidance on how to vote is contrary to their obligation as a fiduciary of the JV?

The table and accompanying guidance must work together in a way that actually works in practice for a company. There are risks of over-defining with whom, when, and how JV Directors must interact to vote on a JV matter. There can be internal political battles over who should decide what. There can be endless debates about what it means to “review” or “consult” versus “approve” or “decide.” After some experience with version one of a JV authorities guidance document, the company may decide decisions are being made too high up in the organization – or too far down. However, these risks can often be managed through a careful development process and by making a guidance document that is fit-for-purpose for the relevant company. After all, only if these risks become larger than the risks of leaving authorities up to individuals should the guidance document be set aside.

~ ~ ~

Ankura and its clients create fit-for-purpose solutions to delegations of authority issues. Whether it means amending an existing DOA policy, making a new one, providing a JV-specific addendum to a DOA policy, or creating a handbook explaining what individuals involved in a JV need to know, we help clients simplify and address how delegations work in a JV context. A thoughtful approach to delegations, paired with strong JV governance, can improve JV performance, reduce risk, and ultimately save both the JV itself and its owners from significant, painful, and costly mistakes.

To learn more about how Ankura advises clients on JV and partnership transactions, governance, restructurings, and exits, please contact James Bamford james.bamford@ankura.com or Tracy Branding Pyle tracy.pyle@ankura.com.

MIT Sloan Management Review, 2022

Businesses are increasingly partnering to meet their strategic objectives — but neglecting governance puts JVs and their shareholders at risk…

Harvard Law School Forum on Corporate Governance, 2019

The governance of public companies is profoundly important. Thirty years ago, CalPERS, a major institutional investor and leading corporate…

Harvard Law School Forum on Corporate Governance, 2020

Twelve years ago, we co-authored with CalPERS a set of guidelines for joint venture governance. At the time we argued, and still believe…

MIT Sloan Management Review, 2021

Taking a minority stake in a joint venture (JV) can make good business sense. What doesn’t make sense is ceding more control than you have to…

Oil & Gas Financial Journal, 2017

The Joint Venture Alchemist, 2020

A decade ago, we established a set of objective tests to allow companies to calibrate how well they are governing their portfolios of joint ventures…

The Joint Venture Alchemist, 2017

It’s time to raise the bar on JV governance. Doing so demands operationalizing the legal agreements and aligning the shareholders on how…

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.

Comments